Design Principles of Referrals Schemes

The Quality versus Quantity Tradeoff

Every referral program faces the same tradeoff: quality versus quantity. Each lever you adjust, be it reward amounts, qualification criteria or even onboarding friction, will have an impact on this balance.

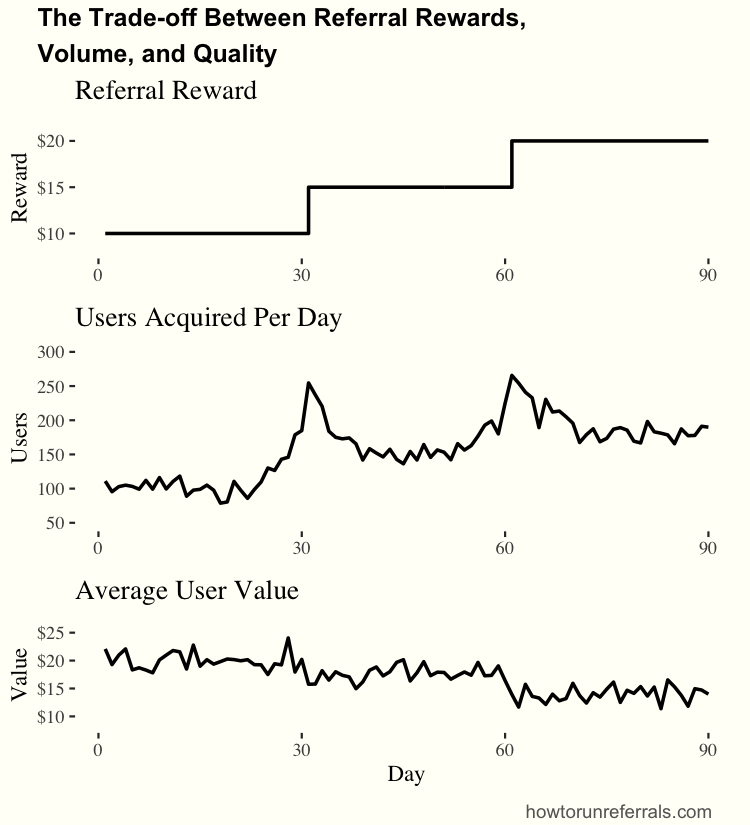

A typical example can be seen below:

The key intuition is that the less incentive (or more friction) there is for people to refer, the better quality the of the users acquired through the acquisition channel will be. If referring is difficult and is unincentivised, only your most loyal users will refer, and they too will only refer people for whom they know the product is a good match. On the other hand, if referring is easy and highly incentivised, your users may be driven to make money by referring customers who are unlikely to be good clients.

Rewards

The more you pay out the more users you acquire. Like for all channels, the relationship between payouts and user acquisition increases linearly at first, and then tends to tail of as the incremental cost per new customer rises.

Moreover, if you increase rewards you tend to find that the average quality of an acquired user goes down. This is because you get a larger percentage of “reward chasers” rather than genuine, interested users of the platform. A lot of running a RAF campaigns has to do with being successful in scaling volumes while not compromising on quality.

Rewards: Cash vs Non-cash Incentives

Casual gaming companies like CandyCrush, Monopoly Go or DuoLingo tend to offer non-cash incentives for their referral schemes. If the average LTV of their users is less than $1, then it is impractical to offer cash incentives for referrals. Instead, they tend to offer non-cash incentives like in-game currency, extra lives and premium product features to entice users to refer new customers.

The advantages of non-cash incentives are that they tend to attract high quality customers, have low marginal costs and have far lower transaction costs than cash incentives. Moreover, in cases when cash incentives are not an option due to low LTVs or regulatory reasons (such as for example cash-incentivised referrals payouts for CFD products, which are banned in the European Union), non-cash incentives allow products to run referrals campaigns.

The disadvantage of non-cash incentives is that they can be hard to stack and thus to scale. If you give a user a free premium feature for referring a customer, what incentive will they have to refer more than one? Moreover, you will get a selection effect in a way that you do not with cash incentives. $50 is $50 for everyone, but your premium feature may be more attractive for some users than others. This is of particular concern with the referee. Even if the referrer values the “extra life” in a game they receive as a reward for onboarding their friend, it is unlikely the referee will value it as highly.

Revoluts ran a non-cash incentive scheme for their metal card

Revoluts ran a non-cash incentive scheme for their metal card

Cash incentives (or at least incentives with a clear monetary value) tend to lead to greater volume because they are more attractive to both referrer and referee, and because they are infinitely stackable. By stackable I mean that if you get 50 dollars for referring a friend, and you refer 5 friends, then 250 dollars is 5 times better than 50. However, they do attract certain people who want to take the money and run.

Rewards: Splitting Rewards

The industry has converged towards the best practice of offering both users a reward. Moreover, the referrer and the referee tend to get an equal sized reward. The reason for this is more psychological than economic. It turns out users are much more likely to want to give a “gift” to their friends than to be seen to be “making money” off a friend.

Uneven sided referral programme by OnePay

Uneven sided referral programme by OnePay

That being said, while it is best practice for most products it is by no means inevitable for it to be like this. Single sided referrals programmes also work, and may even be somewhat more effective depending on the user group. Generally, cash strapped users (such as those using OnePay), or users who refer people who are less close to themselves (e.g. micro-influencers), may want to help themselves to a larger percentage of the reward.

Rewards: Variable vs Non-Variable

Generally, rewards ought to be as simple as possible. The more you increase the complexity of the reward, the harder it is for the referrer to explain and for the referee to understand. The only reason why you would increase complexity is to make the scheme easier to market.

We know that the higher the reward you advertise, the more volume of referrals you get. One way in which you can advertise a high reward without compromising profitability is by offering variable rewards. For example, take Robinhood’s referrals programme. Their terms and conditions tells us that:

The cash value you receive could be anywhere between $5 and $200. Keep in mind, approximately 99% of customers will get stock worth $5. You can use this reward to claim a fractional share of a stock.

Why would Robinhood do this? The hope is that the prospective (or existing) user will read the high number and be anchored towards it. In other words, variable rewards are a way of being able to market potential rewards to users and assume that they will either not read carefully or will “hope” for the big reward.

In an interview, Robinhood employees claim they have AB tested dozens of different reward schemes and have yet to find something more effective than this. Nevertheless, the option might not be available to everyone given compliance limitations, and it is probably more suitable to some products than others.

Rewards: Cliffs, Bonuses and Limits

Another way in which you can market a higher number is by introducing limits, cliffs or bonuses that make “real” payouts smaller than “marketing” figures.

An important thing to realise is that the user often has limited control over how many users they refer. They can invite a friend, but whether they sign up and they meet the qualification criteria or not is often beyond their control. Their friend may be too lazy to sign up, or might not understand your app. For this reason, varying the value paid out based on the number of people they refer can be another way in which you can introduce variance into payout amounts.

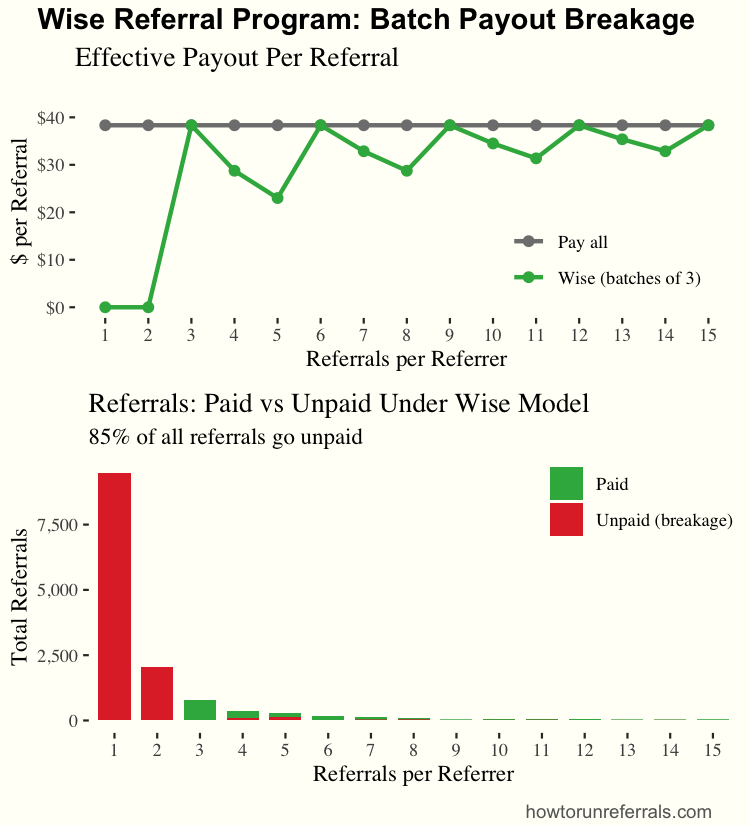

For example, Wise’s campaign offers a payout ONLY if the user refers three individual separate new clients. This introduces breakage, which means that a lot of referrals will not get paid out ever. The purpose of this is to save on costs. The image below illustrates just how much:

Assuming a distribution of referees per referrer, Wise can cut costs by up to 90% through this payout scheme.

Another option is to limit the amount of users a single individual can be paid for. This also serves as a cost saving measure, but can help limit fraud and removes incentives for abuse too.

One of the best tactics I have found is to add a bonus incentive for the first referral. Referrers tend to refer multiple people, knowing that there is no guarantee any particular user will convert. By paying double for the first referral, you often can buy multiple referrals at a good price. Moreover, it makes it more likely for an individual to make their first referral, which increases the amount of referrals considerably.

On The Qualification Criteria

add images to illustrate

Examples of qualification criteria:

- Capital.com: 200 USD deposit and 3 trades

- Wise: three friends who do X

- Public.com: Buy 1000 worth of stocks

The reason why you are setting up qualification criteria for a referred user to hit is because you want to make sure you are getting a valuable user for your money. Here too you have to balance on the quality vs quantity tradeoff.

If you make it a bit too easy to meet the criteria, you’ll end up flooded by users who simply to take your money. If you make it too hard, you’ll end up acquiring very few incremental new users. Tightening the quality criteria is often analogous to paying less. You’ll acquire fewer users, but of average better quality.This is not always true, but most of the time it is.

A good qualification criteria is generally a heuristic that predicts a high user lifetime value.

My favourite qualification criteria was the one we used at Zilch. We ran a simple regression that showed that adding a card to a mobile wallet was one of the best predictors of higher user LTV. We realised that once a user added a Zilch card to their device wallet, it was very sticky. Very few users would go through the effort of deleting the card, which meant that sooner or later they were likely to use it.

Our qualification criteria then became: “The new user must spend using ApplePay / GooglePay to get your rewards”. We even made the referrer rewards only spendable via mobile wallet, ensuring both users were more likely to be retained.

The qualification criteria should “predict” LTV, not “be” LTV. There is sometimes a temptation to try to keep qualification criteria tight, effectively turning referrals rewards into a fee rebate. For example, a business will calculate that $100 in user spend generates $30 in profit, so they will “give” back some of the profit (i.e 30 USD) to the user. The argument is sometimes made that this will make abuse and fraud impossible. I generally advise against this, because most users can see through the transactional nature of this arrangement. They want a reward in anticipation of their business, not a discount on existing transactions.

Make the criteria as simple as possible. Not only do your referrers need to be able to understand it, they also need to be able to explain it to the referees, who understand your product even less than they do. Do not use internal jargon (“registered customer”, “lead”, etc) and assume the user will understand. Along these lines, a good qualification criteria needs to seem easy to do. It doesn’t necessarily have to be easy, but it needs to seem simple enough to the user. A good example of this is Robinhood’s ‘invite a friend and link a bank account to get a stock’. This seems easy enough to do, but does not say anything about risk checks, KYC verification, eligibility questionnaires and other things which might be necessary to link an account.

Qualification: Time Limits and Limited Time Offers

Like in the Revolut example above, often referrals programmes will introduce limited time offers with a higher bonus structure than before. This serves two purposes, first to give people an incentive to refer now as opposed to procrastinating and deferring it to some endless point in the future. Instilling a sense of urgency for action is key.

Second, it can be used to manage flows and campaigns. Because referrrals campaigns can have uncertain outcomes (e.g. due to the introduction of a new qualification criteria or a higher reward) limiting the duration of the campaign can limit the potential cost of a campaign. If from outset the campaign is set to expire after a limited amount of time, you can avoid changing terms and conditions on users at the last minute. If the new offer is for unlimited time, the campaign could easily grow more than expected and would potentially acquire a cohort of low value customers. By limiting the duration of the campaign, it allows for a manageable post-campaign analysis to review the cohort’s value.

Third, it can help capitalise on certain events or seasonality. A “Christmas campaign” may encourage people to share the product with their families when they are at home.

Referrals UI - UX

comment: draft, bring up to speed with examples from the site where you need to pay, add ALEX’s comments here maybe? A well-designed refer-a-friend scheme has the following elements:

- Referral hub / entry point The main screen where you land. Shows your unique link or code, maybe a headline like “Earn £50 per friend.” Often has a prominent share button and a summary of your stats (invited: X, earned: £Y).

- Share/invite screen Where you actually distribute the link. Usually presents options: copy link, share via WhatsApp, SMS, email, social media. Sometimes includes a QR code. Revolut does this as a modal; Wise keeps it inline.

- Status tracker Shows progression of each referral. Typically columns or cards with states like: “Invited” → “Signed up” → “Completed action” → “Reward unlocked.” This is where users check if their friend actually qualified.

- Rewards / earnings screen Your payout history and pending amounts. Shows what you’ve earned, when it was credited, and any rewards still waiting to unlock. PayPal tends to show this as a transaction-style list; Revolut uses a more visual summary.

- Terms / how it works Explains qualification criteria. What counts as a “qualifying action”—first transfer, card spend, verification, etc. Usually a separate detail page or expandable section.

Omitting any of these pages is asking for trouble later. If you don’t have a “status tracker” for example, your customer support will be inundated with people asking.